AI-POWERED BROKER PROSPECTING SYSTEM

From 100:1 Cold Calls to a Precision Broker Intelligence System

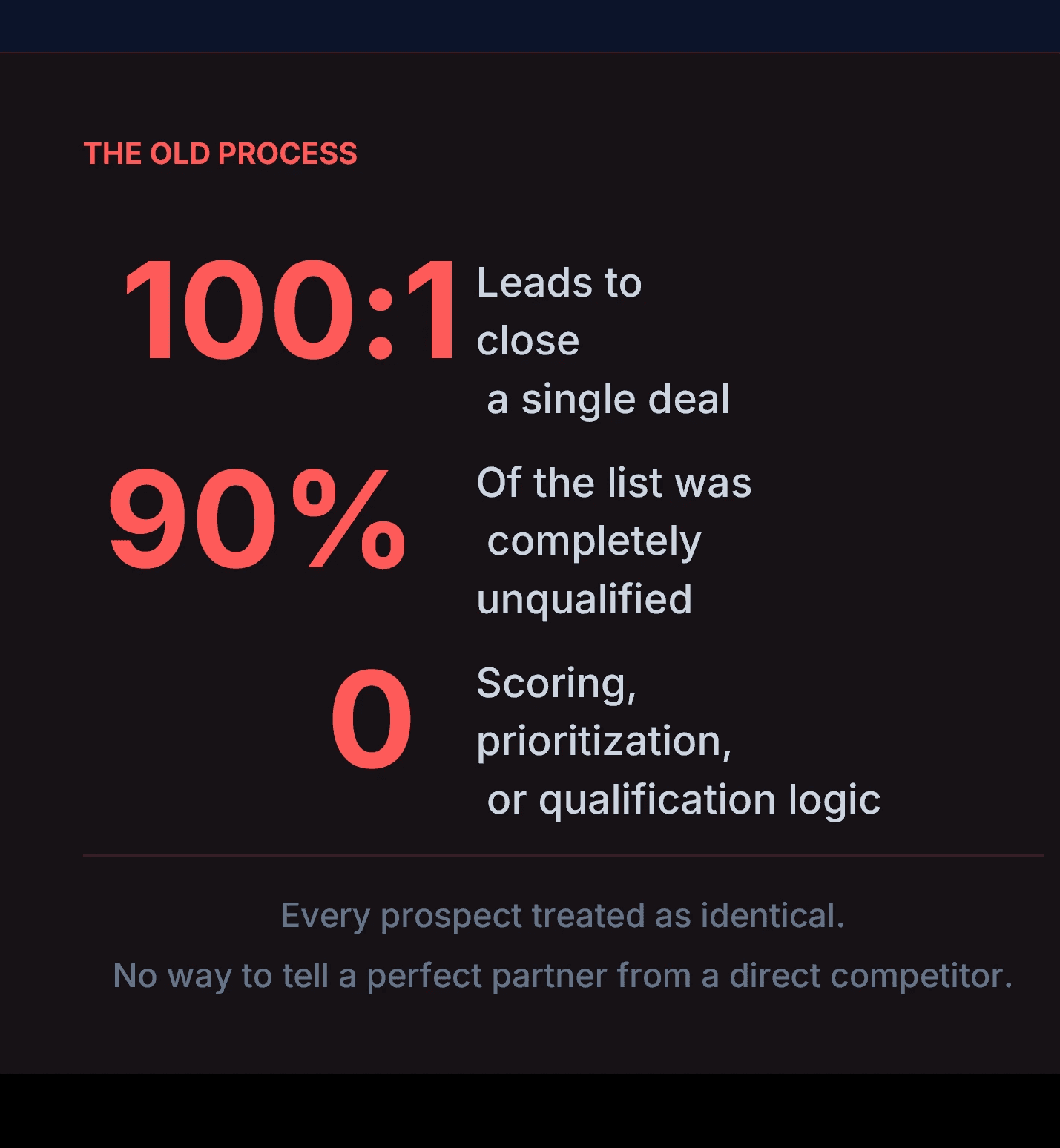

The Challenge — When Title Tells You Nothing: The ICP Surfacing Problem No Data Provider Solves

A US-based private lending company funds residential investment loans. Their growth model depended on recruiting independent mortgage brokers as white-label distribution partners -- brokers originate loans under their own brand while the company provides the capital.

The sales team was cold-calling from purchased lists with no qualification layer. The results reflected the approach: a 100:1 lead-to-deal ratio, with 90% of prospects fundamentally unable to become partners regardless of how well the pitch landed.

The problem was not the sales team. It was the list. But replacing the list would not have solved it either. On LinkedIn, the same problem exists: "Mortgage Broker" and "Loan Officer" cover independent investment-property specialists and bank employees focused on FHA loans in equal measure. Title tells you almost nothing about business model. A contact who added 5,000 mortgage professionals on LinkedIn would face the exact same wall -- the signal simply is not in the title.

The core issue was ICP definition and surfacing, not volume. In this industry, identical titles hide completely different business models, and no standard data provider surfaces the distinction.

The Approach: Rebuild the Prospecting Logic

Rather than sourcing a better list, I rebuilt the prospecting logic from the ground up, starting with what signals actually differentiate a recruitable broker from an unqualifiable one.

Step 1: ICP Decomposition

The client's initial ICP was simply "mortgage brokers." Through stakeholder interviews, I decomposed this into a precise set of qualifying and disqualifying signals based on their actual business model:

Company type: independent broker or boutique shop vs. large retail bank or national lender

Product focus: investment property lending (DSCR, fix & flip, bridge, hard money, non-QM) vs. consumer-only (FHA, VA, primary residence)

Business model: brokers who distribute through capital partners vs. direct lenders funding their own capital

Activity level: active originator with current deal flow vs. dormant license

Geography: licensed in target states vs. excluded territories

The competitor distinction was the most critical and least obvious signal. Several prospects appeared to be strong partners but were actually direct lenders funding their own capital -- making them competitors, not distribution partners. No standard data provider surfaces this distinction because it requires understanding business model, not just matching keywords.

Step 2: AI Scoring Engine

Built a Clay workflow that sources broker prospects via Clay Find People, filtered by job title and investment-lending keywords, then enriches each record with company data and biographical details from LinkedIn. An AI scoring prompt evaluates every prospect against the ICP criteria and outputs a score of 1 to 4 with a written rationale.

The critical insight came from prompt iteration, not just prompt design. The first prompt matched keywords -- it saw "fix and flip" and "hard money" and called it a strong fit. The second prompt understood business models. Same prospect, same data -- score dropped from a 3 to a 1. Because the company description said "direct private lender, funded over 1,600 loans." That is a competitor, not a distribution partner. Keywords could not catch that distinction. Business logic could.

Score 4: Independent shop, explicit investor-lending signals, active originator -- immediate outreach

Score 3: Strong fit, investment property focus without full signal match -- priority outreach

Score 2: Possible fit, small firm but bio lacks investor-lending signals -- verification layer

Score 1: Large bank employee, consumer-only focus, direct lender, or commercial broker -- auto-filtered

The system is also designed around cost efficiency: free formula filters run first, AI scoring only fires where judgment is needed, and expensive web research only triggers on high-scoring rows.

Step 3: Claygent Verification

High-scoring prospects go through a Claygent verification layer that visits company websites to confirm whether they broker loans or fund their own capital -- the distinction that keyword matching cannot reliably make.

Every failure mode is accounted for and routed deliberately: a confirmed broker model passes through, a parked domain routes to manual review, a blocked site routes to manual review. The system is designed so that no false positive reaches the outreach pipeline.

Step 4: Personalized Outreach Preparation

Approved prospects receive a one-line personalized opener referencing something specific from their profile. The scoring tells the rep who to contact. The approach field tells them how. The handoff to sales is not a list -- it is a prioritized, contextualized queue

22 prospects scored, validated, and dispositioned in the Florida pilot

2 fully approved with personalized outreach ready at delivery

70% improvement in valid lead rate

Research time reduced from 3 hours to 3 minutes per account

4-tier AI scoring with written rationale for every prospect

First deliverable within 2 weeks

45+ states in expansion pipeline, with scoring prompt refined per batch based on client feedback

The gap between "using Clay" and "building a prospecting system" is the gap between having a spreadsheet and having a financial model. The tool is necessary but not sufficient.

The value lives in ICP decomposition, scoring logic design, prompt iteration, and the ability to translate a client's business model into signals that an AI can evaluate consistently. The jump from prompt version one to prompt version two -- from keyword matching to business model reasoning -- is where most of the intelligence lives. That is not a Clay skill. That is a systems thinking skill.

In an industry where title standardization actively obscures business model, the surfacing problem cannot be solved at the data layer. It has to be solved at the logic layer.

The scoring process also surfaced a strategic reframe for the client's outreach: the most effective pitch was not "we offer private lending" but "we can help you add a private lending product line to your business under your own brand, with no capital required." This reframe -- from vendor pitch to business expansion opportunity -- emerged directly from understanding which broker signals correlated with partnership readiness. That kind of insight only becomes visible once the ICP is properly decomposed.